Canadians often find themselves in the top 10, but never first:

- Winter Olympics Gold Medals (5th)

- Gross Domestic Product (9th)

- Quality of Life (3rd)

- Oil Reserves (3rd)

- Largest Amount of Uninhabited Land (6th)

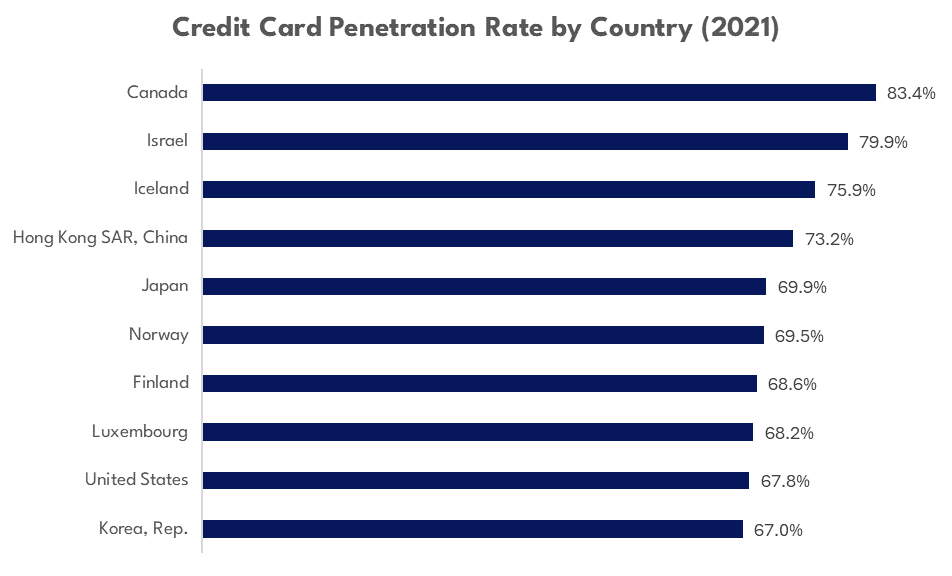

Today, we’ve found something that Canada finally ranks first in, credit card penetration rate at a whopping 83%! But, why is this the case? Is it even a good thing? Let’s explore.

Source: The World Bank

Before we talk about why, let’s first clarify what this means. These figures demonstrate the percentage of the population of each of these countries (above the age of 15) that own a credit card. In fact, if we measured above the age of 18 instead, Canada’s penetration rate would get boosted to 93% (Government of Canada).

Now that we have the “what” cleared up, let’s discuss why:

Banking System Structure

Consolidated Banking

Canada’s banking industry is highly concentrated, with the Big Five banks dominating the market. These banks not only provide a full range of financial services but also maintain deep, trusted relationships with their customers. This strong relationship makes it easier for banks to cross-sell credit cards as part of their overall service offerings.

A typical Canadian might open a checking account with RBC and be offered a credit card as part of their account package, often with incentives such as waived fees for the first year.

Universal Banking Services

In Canada, it’s common for banks to offer bundled services, where customers can access checking accounts, savings accounts, loans, and credit cards all in one place. This integrated approach simplifies financial management and encourages customers to adopt multiple products from the same institution, including credit cards.

In contrast, countries like Japan (69.8%) have a more fragmented banking system, where consumers might use separate institutions for different financial services, leading to lower credit card adoption rates.

High Credit Card Rewards

Attractive Rewards Programs

Canadian credit cards are known for their competitive rewards programs, including cashback, travel points, and retailer-specific perks. These rewards programs are particularly appealing in a country where cross-border shopping with the United States is common. The ability to earn points that can be redeemed for flights, hotel stays, or even cash makes credit card usage highly attractive.

The American Express Cobalt Card, popular in Canada, offers significant rewards on dining and travel, with points that can be used across various travel platforms, making it a favorite among young professionals.

Cross-Border Shopping

Given Canada’s proximity to the United States, many Canadians frequently shop across the border, either in person or online. Credit cards offer convenience and favorable exchange rates compared to cash, making them the preferred payment method.

In countries like Germany, there is a stronger cultural preference for cash transactions, even when traveling abroad. This cultural difference contributes to Germany’s lower credit card penetration rate (60.9%).

Cultural and Economic Factors

Consumer Culture

Canada shares a consumer culture similar to that of the United States, where credit cards are not only normalized but also encouraged. Credit cards are seen as a convenient and secure way to make transactions, both in-store and online. This cultural acceptance is reinforced by aggressive marketing campaigns by banks and financial institutions, making credit card ownership a societal norm.

Advertisements for credit cards featuring zero-interest promotional periods or lucrative sign-up bonuses are common across Canadian media, further embedding the credit card culture in Canadian society.

Access to Credit

Canada’s relatively high GDP per capita and stable economy ensure that a large portion of the population qualifies for credit cards. Moreover, Canadians generally have a good understanding of credit and financial literacy, which promotes responsible credit card use. Financial literacy programs in schools and community organizations further bolster this understanding.

In contrast, many developing countries have lower access to credit due to economic instability and a lack of financial literacy programs, resulting in lower credit card penetration rates.

Government and Regulatory Environment

Consumer Protection Laws

Canada’s strong consumer protection laws regulate interest rates, fees, and other aspects of credit card usage. These protections make consumers feel more secure using credit cards without the fear of being exploited by predatory practices.

The Canadian government’s regulations on maximum interest rates ensure that even subprime borrowers are protected from excessive charges, unlike in some other countries where interest rates can be exorbitant.

Emphasis on Credit History

Building and maintaining a good credit history is crucial in Canada, particularly for accessing financial products like mortgages and loans. As a result, many Canadians start using credit cards early in life to build their credit scores, viewing them as an essential tool for long-term financial planning.

In countries like France, there is less emphasis on personal credit scores for financial products, leading to a lower credit card penetration rate. Instead, personal loans and bank overdrafts are more commonly used.

Technological Adoption

Advanced Payment Infrastructure

Canada boasts a highly developed payment infrastructure that supports widespread acceptance of credit cards. The availability of contactless payments, mobile wallets, and robust online banking systems makes credit cards a convenient option for everyday transactions.

Nearly every retailer in Canada, from large department stores to small local businesses, accepts credit cards, and the adoption of contactless payments has surged, especially during the COVID-19 pandemic.

High Internet Penetration

Canada’s high level of internet penetration supports a thriving e-commerce environment, where credit cards are the dominant method of payment. The convenience of online shopping and the necessity of using credit cards for these transactions contribute significantly to the high penetration rate.

In countries with lower internet penetration, such as India (2.4%), cash-on-delivery remains a popular option for online shopping, leading to lower credit card usage overall.

Financial Inclusion

Widespread Financial Access

In Canada, a significant portion of the population has access to banking services, including credit cards. This financial inclusion is facilitated by the country’s robust banking network, which reaches even remote areas, ensuring that most Canadians can access credit services.

Even in rural areas of Canada, residents have access to banking services through local branches, ATMs, and online platforms, making credit card ownership accessible to nearly everyone.

Government Benefits and Subsidies

Some government benefits and subsidies in Canada are linked to banking services, which indirectly encourages the use of credit cards. For instance, certain tax rebates and incentives are easier to claim when linked to a bank account, encouraging greater interaction with the financial system.

In contrast, in many African countries, where large portions of the population remain unbanked, mobile money services have become more popular than traditional banking services, resulting in lower credit card penetration.

Comparison with Other Countries

Cultural Differences

In many countries, cultural preferences lean towards using cash or debit cards over credit cards. For example, in Japan, there is a strong cultural emphasis on avoiding debt, which leads to a preference for cash and debit transactions. This contrasts sharply with the Canadian approach, where credit cards are viewed as a practical financial tool rather than a source of debt.

In Germany, the “Schwarz Null” or “Black Zero” policy reflects a cultural preference for saving and avoiding debt, which aligns with the lower use of credit cards in favor of cash or direct debit transactions.

Economic Instability

In some countries, economic instability or high inflation rates create a mistrust of credit products, resulting in lower credit card penetration rates. In places like Argentina (23.3%), for example, rampant inflation has led to a reliance on cash and alternative payment methods rather than traditional credit cards.

Canada’s stable economy and low inflation rates create an environment where credit cards are seen as safe and reliable, further contributing to their widespread use.

Conclusion

The high penetration rate of credit cards in Canada is the result of a complex interplay of factors, including a consolidated banking system, attractive rewards programs, a consumer culture that embraces credit, robust consumer protection laws, and advanced payment infrastructure. Compared to other countries, where cultural preferences, economic conditions, or regulatory environments might inhibit credit card adoption, Canada stands out as a nation where credit cards are not just common, but a deeply embedded part of everyday life.

This unique combination of factors makes Canada an interesting case study in understanding global financial behavior and the varying approaches to credit around the world.

Leave a Reply